PUBLIC BANK BERHAD (PBBANK 1295)

SNAPSHOT

| YE 31-Dec | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| Profit Before Tax (RM mil) | 6,285 | 7,367 | 8,831 | 8,539 | 8,932 | 9,543 |

| Net Profit After Tax (RM mil) | 4,872 | 5,657 | 6,119 | 6,649 | 7,147 | 7,224 |

| EPS (RM) | 0.251 | 0.2914 | 0.3153 | 0.3426 | 0.3684 | 0.374 |

| DPS (RM) | 0.13 | 0.152 | 0.17 | 0.19 | 0.21 | 0.23 |

| Net Loans (RM mil) | 342,803 | 354,053 | 372,583 | 394,750 | 420,472 | 442,333 |

| Customer Deposits (RM mil) | 365,871 | 380,394 | 394,718 | 412,897 | 433,264 | 447,114 |

| Shareholders Funds (RM mil) | 47,248 | 48,163 | 50,179 | 54,674 | 57,335 | 59,938 |

| Net Assets / Total Assets (%) | 10.7% | 10.7% | 10.4% | 11.0% | 11.0% | 11.1% |

| NTA per share (RM) | 11.55 | 2.35 | 2.45 | 2.68 | 2.81 | 2.93 |

| No of Shares (millions) | 3,882.1 | 19,411 | 19,411 | 19,411 | 19,411 | 19,411 |

| Share Price – Close (RM) | 20.60 | 4.16 | 4.32 | 4.29 | 4.56 | 4.54 |

| Financial Ratios (%) | ||||||

| Return on Av Equity | 10.7% | 11.9% | 12.4% | 12.7% | 12.8% | 12.3% |

| Cost to Income Ratio | 34.6% | 31.6% | 31.5% | 33.7% | 34.5% | 35.6% |

| Loan to Deposit Ratio | 94.5% | 94.1% | 95.5% | 96.6% | 97.9% | 99.7% |

| Impaired Loans | 0.8% | 1.1% | 1.1% | 1.1% | 0.9% | 0.8% |

| Net Interest / Total Interest Income | 50.6% | 61.7% | 61.4% | 50.2% | 50.1% | 51.0% |

| Interest Income / Av Net Loans | 4.23% | 3.87% | 4.11% | 4.70% | 4.63% | 4.38% |

SHARE TRADING SUMMARY CY2025

| Share Price - High | RM4.70 |

| Share Price - Low | RM4.03 |

| Share Price - Close @ 31/12/25 | RM4.54 |

| Average Daily Volume | 16,932,838 shares |

| Volume - High | 67,040,797 shares |

| Volume - Low | 3,001,900 shares |

| Total Annual Volume | 4,131,612,492 shares |

|

Annual Turnover (% of Share Capital) |

21.3% |

TOP SHAREHOLDERS

| As at 27 February 2026 | Direct | Deemed |

| Estate of the late Tan Sri Teh HP | 0.64% | 21.38% |

| Consolidated Teh Holdings Sdn Bhd | 21.38% | - |

| Employees Provident Fund Board | 17.97% | - |

| Kumpulan Wang Persaraan (Diperbadankan) | 4.86% | 0.23% |

| Total | 44.85% |

KEY STRENGTHS

Public Bank is a market leader in retail banking in Malaysia. For the year ending 31/12/24, Retail Banking Operations generated RM4.4 billion in Profit Before Tax (PBT), which is surpassed only by Maybank’s Community Financial Services segment which generated RM6.2 billion PBT for the same period, while ahead of CIMB Group’s Consumer Banking segment at RM2.8 billion PBT. Through its 100% owned subsidiary Public Mutual Berhad, Public Bank is Malaysia’s market leader in Funds Management with more than RM100 billion in Assets Under Management, generating RM798 million PBT for the group.

Public Bank is a relatively small player in commercial and investment banking and its overseas earnings is mainly through Public Bank Cambodia which generated a relatively modest RM342 million in PBT for 2023.

“If a shareholder of Public Bank bought 1,000 shares in 1967 when Public Bank was listed, and assuming that the shareholder subscribed to all rights issues and did not sell any of the shares, he would have accumulated 744,690 shares worth RM3.2 million based on Public Bank’s share price of RM4.29 as at the end of 2023. In addition, he would have received a total gross dividend of RM1.9 million whilst having only invested a capital outlay of RM235,612, including subscription for all rights issues. Total dividends received and appreciation in share value translate to a remarkable compounded annual rate of return of 17.7% for each of the 56 years that this shareholder has held the share in Public Bank since it was listed in 1967.”

Source: Public Bank Berhad 2023 Annual Report (Page 65)

SEGMENT EARNINGS (RM mil)

| FY 2024 | FY 2025 | |

| Hire Purchase | 1,048 | 665 |

| Retail Operations | 4,446 | 4,677 |

| Corporate Lending | 843 | 851 |

| Treasury & Capital Markets | 290 | 308 |

| Investment Banking | 93 | 65 |

| Funds Management | 860 | 851 |

| Others | 33 | 394 |

| Head Office & Funding | 1,209 | 1,224 |

| Hong Kong | (594) | 65 |

| Cambodia | 374 | 300 |

| Other Countries | 89 | 87 |

| Associates | 241 | 56 |

| Profit Before Tax | 8,932 | 9,543 |

LOAN SEGMENTATION

FINANCIALS

|

(RM '000) Year Ending |

2023 31-Dec |

2024 31-Dec |

2025 31-Dec |

| Revenue | 25,415,010 | 27,205,162 | 29,509,548 |

| Interest Income | 18,040,197 | 18,871,101 | 18,895,780 |

| Interest Expense | (8,984,905) | (9,419,995) | (9,312,094) |

| Net Interest | 9,055,292 | 9,451,106 | 9,583,686 |

| Islamic Banking Income | 1,561,548 | 1,707,000 | 1,839,388 |

| Insurance Service Result | 0 | 35,434 | 347,677 |

| Net Finance Expense from Insurance Contracts | 0 | (6,246) | (40,542) |

| Other Operating Income | 2,475,747 | 2,823,380 | 2,964,945 |

| Other Operating Expenses | (4,414,788) | (4,828,132) | (5,128,702) |

| Impairment on Loans, Advances and Financing | (156,689) | (565) | (66,830) |

| Impairment on Other Assets | (1,278) | (491,511) | (12,790) |

| Share of Results of Associates & JV | 18,956 | 241,163 | 56,021 |

| Profit Before Tax from Continuing Operations | 8,538,788 | 8,931,629 | 9,542,853 |

| Tax Expense | (1,883,775) | (1,912,565) | (2,135,744) |

| PAT from Continuing Operations | 6,655,013 | 7,019,064 | 7,407,109 |

| Profit After Tax | 6,655,013 | 7,019,064 | 7,407,109 |

| Non-Controlling Interests | (5,699) | 127,967 | (182,687) |

| Net Profit After Tax | 6,649,314 | 7,147,031 | 7,224,422 |

| EPS Basic / Diluted (sen) | 34.26 | 36.84 | 37.41 |

|

(RM '000) Year Ending |

2023 31-Dec |

2024 31-Dec |

2025 31-Dec |

| Net Loans | 394,749,979 | 420,471,698 | 442,333,231 |

| Cash & Deposits with Financial Institutions | 11,127,417 | 15,468,967 | 16,828,730 |

| Fin Assets (FVPL) | 2,637,648 | 4,001,101 | 3,978,524 |

| Fin Assets (FVCI) | 54,138,308 | 53,918,467 | 50,198,502 |

| Fin Investments (Amortized) | 29,955,413 | 29,003,179 | 30,821,009 |

| Derivative Financial Instruments | 414,811 | 568,069 | 224,574 |

| Statutory Deposits | 7,526,753 | 7,650,252 | 4,441,274 |

| Intangible Assets | 2,589,600 | 2,799,350 | 3,085,617 |

| Right-Of-Use Assets | 1,243,436 | 1,225,507 | 1,215,244 |

| Associates & JV | 141,743 | 384,051 | 441,227 |

| Other Assets | 6,072,889 | 7,372,437 | 8,083,225 |

| Total Assets | 510,597,997 | 542,863,078 | 561,651,157 |

| Deposits from Customers | 412,896,967 | 433,264,270 | 447,113,622 |

| Deposits from Financial Institutions | 12,602,429 | 13,457,604 | 14,625,343 |

| Obligations on Securities Sold under Repurchase Agmts | 3,017,789 | 8,129,570 | 5,624,576 |

| Bills and Acceptances Payable | 192,169 | 263,403 | 155,667 |

| Recourse Obligations on Loans Sold to Cagamas | 5,100,015 | 5,000,015 | 6,200,017 |

| Derivative Financial Liabilities | 354,450 | 353,146 | 641,642 |

| Insurance Contract Liabilities | 0 | 2,256,984 | 2,387,044 |

| Debt Securities & Borrowings | 11,144,016 | 11,014,507 | 12,649,937 |

| Lease Liabilities | 904,324 | 918,482 | 906,189 |

| Other Liabilities | 8,005,720 | 8,558,107 | 8,905,512 |

| Total Liabilities | 454,217,879 | 483,216,088 | 499,209,549 |

| NET ASSETS | 56,380,118 | 59,646,990 | 62,441,608 |

| Share Capital | 9,417,653 | 9,417,653 | 9,417,653 |

| Retained Profits | 42,447,124 | 44,811,446 | 47,205,232 |

| Regulatory Reserves | 723,829 | 1,591,435 | 2,257,273 |

| Treasury Shares | 0 | (434,752) | (434,752) |

| Other Reserves | 2,085,743 | 1,949,712 | 1,492,268 |

| Shareholder Funds | 54,674,349 | 57,335,494 | 59,937,674 |

| Non-Controlling Interests | 1,705,769 | 2,311,496 | 2,503,934 |

| TOTAL EQUITY | 56,380,118 | 59,646,990 | 62,441,608 |

| No of Shares (Thousands) | 19,410,692 | 19,410,692 | 19,410,692 |

| Weighted Av Shares (Thousands) | 19,410,692 | 19,402,454 | 19,313,432 |

|

(RM '000) Year Ending |

2023 31-Dec |

2024 31-Dec |

2025 31-Dec |

| Profit Before Tax | 8,538,788 | 8,931,629 | 9,542,853 |

| Non-Cash Items (Depreciation, Share of Associates, Loan Impairments & Other Items) | 667,523 | 707,861 | 407,821 |

| Operating Profit Before Working Capital Changes | 9,206,311 | 9,639,490 | 10,013,674 |

| Loans, Advances and Financing | (22,592,185) | (25,909,832) | (22,132,866) |

| Movement in Other Operating Assets | (845,352) | (145,042) | 3,101,722 |

| Deposits from Customers | 18,178,210 | 20,367,303 | 13,849,352 |

| Movement in Other Operating Liabilities | (4,441,026) | 6,329,814 | 787,394 |

| Income Tax Expense and Zakat Paid | (2,345,300) | (2,052,094) | (2,007,768) |

| Other Operating Items | 3,342 | 24,881 | (70,327) |

| Cash Flow from Operating Activities | (2,836,000) | 8,254,520 | 3,541,181 |

| Net Purchase of Property Plant & Equipment | (306,732) | (182,534) | (266,402) |

| Net Sale/(Purchase) of Fin Investments | (2,889,644) | 1,609,730 | 2,426,196 |

| Acquisition of Subsidiaries | - | (1,504,980) | - |

| Other Investing Items | 353,655 | (74,363) | 12,548 |

| Cash Flow from Investing Activities | (2,842,721) | (152,147) | 2,172,342 |

| Dividends Paid to Shareholders | (2,717,497) | (3,882,138) | (4,152,388) |

| Dividends Paid to Non-Controlling Interests | (6,872) | (10,161) | (172,754) |

| Repayment of Lease Liabilities | (87,443) | (89,808) | (96,605) |

| Net Issuance/(Redemption) of Debt Securities | (1,011,155) | (1,620) | 2,508,584 |

| Repayment of Other Borrowings | - | - | (626,822) |

| Cash Flow from Financing Activities | (3,822,967) | (3,983,727) | (2,539,985) |

| Net Cash Flow | (9,501,688) | 4,118,646 | 3,173,538 |

| Effects of Exchange Rate Changes | (1,569,269) | (432,703) | (1,136,026) |

Income & Cost Metrics

| Year Ending |

2023 31-Dec |

2024 31-Dec |

2025 31-Dec |

| (RM'000) | |||

| Interest Income | 18,040,197 | 18,871,101 | 18,895,780 |

| Interest Expense | (8,984,905) | (9,419,995) | (9,312,094) |

| Net Interest | 9,055,292 | 9,451,106 | 9,583,686 |

| Islamic Banking Income | 1,561,548 | 1,707,000 | 1,839,388 |

| Insurance Service Result | 0 | 35,434 | 347,677 |

| Net Finance Expense from Insurance Contracts | 0 | (6,246) | (40,542) |

| Other Operating Income* | 2,475,747 | 2,823,380 | 2,964,945 |

| Total Operating Income | 13,092,587 | 14,010,674 | 14,695,154 |

| Operating Cost** | (4,414,788) | (4,828,132) | (5,128,702) |

| Cost-to-Income Ratio (%) | 33.7% | 34.5% | 35.60% |

| Year Ending |

2023 31-Dec |

2024 31-Dec |

2025 31-Dec |

| *Other Operating Income (RM'000) | |||

| Fee & Commission Income (Net) | 1,949,847 | 2,187,020 | 2,225,565 |

| Realised Gain/(Loss) on Fin Instruments | 70,368 | 47,997 | 174,321 |

| Unrealised Gain/(Loss) on Fin Instruments | (28,569) | 69,908 | (8,553) |

| Dividend Income | 5,235 | 11,141 | 59,834 |

| Foreign Exchange Gain/(Loss) | 360,755 | 392,126 | 412,949 |

| Other Income | 118,111 | 115,188 | 100,829 |

| Total | 2,475,747 | 2,823,380 | 2,964,945 |

| Annual Report Ref (PDF Page) |

Note 33 to 35 (p294-296) |

Note 35 to 37 (p140-142) |

Note 35 to 37 (p152-154) |

| Year Ending |

2023 31-Dec |

2024 31-Dec |

2025 31-Dec |

| **Operating Cost (RM'000) | |||

| Personnel Costs | (3,196,151) | (3,551,060) | (3,696,022) |

| Establishment Costs | (818,156) | (859,457) | (912,335) |

| Marketing Expenses | (109,805) | (122,984) | (145,548) |

| Administration and General Expenses | (290,676) | (294,631) | (374,797) |

| Total Operating Cost | (4,414,788) | (4,828,132) | (5,128,702) |

| Annual Report Ref (PDF Page) | Note 36 (p297) | Note 38 (p143) | Note 38 (p155) |

| Profit Before Tax (RM'000) | 8,538,788 | 8,931,629 | 9,542,853 |

| Personnel Costs / Profit Before Tax (%) | 37.4% | 39.8% | 38.7% |

| Personnel Costs / Operating Cost (%) | 72.4% | 73.5% | 72.1% |

STAKEHOLDERS

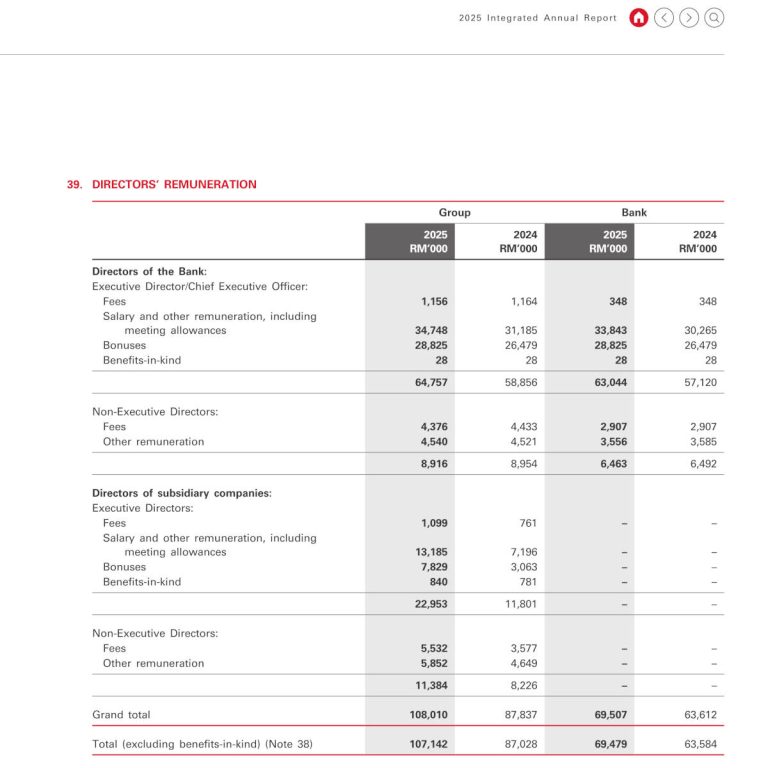

Directors & CEO Remuneration

Executive & CEO: RM64.8 million

Non-Executive: RM8.9 million

Subsidiaries: RM34.3 million

CEO: RM64.8 million

Executive & CEO: RM58.9 million

Non-Executive: RM8.9 million

Subsidiaries: RM20.0 million

CEO: RM58.9 million

Executive & CEO: RM52.8 million

Non-Executive: RM7.9 million

Subsidiaries: RM18.3 million

CEO: RM52.8 million

Executive & CEO: RM46.8 million

Non-Executive: RM29.5 million

Subsidiaries: RM17.7 million

CEO: RM46.8 million

Executive & CEO: RM40.5 million

Non-Executive: RM29.0 million

Subsidiaries: RM16.9 million

CEO: RM40.5 million

Directors & CEO Interests

As at 31/12/24, Public Bank’s CEO and key director, Tan Sri Tay Ah Lek had a stake of 27.44 million shares in the company. This has not changed since 31/12/21. During the financial year ended 31/12/21, he acquired 9.5 million shares in the company. Previously he held 3,688,845 shares and received 14,755,380 bonus shares as a result of the company’s Bonus Issue in FY2021.

CORPORATE DEVELOPMENTS

Selldown of 251 million shares by Consolidated Teh

Following a Restricted Offer for Sale (ROFS) made to directors and employees of the Public Bank Group, Consolidated Teh Holdings Sdn Bhd (ConsTeh) has effectively disposed of 250.913 million shares in Public Bank Berhad on 9 June 2026. This represents a 1.9% of the bank’s share capital. This is in line with the family’s plans to pare down their shareholding in Public Bank to 10% over a five-year period in compliance with the Financial Services Act.

Interestingly, share trading volume spiked to 108.6 million shares on 29 May 2026 closing at RM4.71 with a traded price range of RM4.66 to RM4.79. PBBANK share price has largely fluctuated in the RM4.70 to RM4.90 range in the month of May with an average daily trading volume of 19.9 million shares excluding the unusually large volume on 29 May. The average daily trading volume for 2025 was 16.9 million shares.

(LKFP: If we peg the share price at RM4.80 and apply 7 to 10% discount, it would imply a share price of between RM4.32 to 4.46 per share for this ROFS tranche. Taking the average as a guesstimate, employees are possibly paying RM4.39 per share. There may be some selling pressure from RM4.50 to 4.80 before the market absorbs it.)

Following the disposal, ConsTeh still holds 3,899,767,275 shares or slightly over 20% in the banking group, which means it needs to further divest 2 billion or so shares before end of year 2029.

Selldown of 220.3 million PBBANK shares by LPI Capital Bhd

LPI Capital Bhd has completed the disposal of its remaining shares in Public Bank Berhad (PBBANK) to local and foreign institutional investors, selling 220.3 million shares for RM1.05 billion. This stake represents a 1.1% of PBBANK’s total share capital.

The shares were disposed of at RM4.75 each, being 0.42% discount to PBBANK’S closing price of RM4.77 on May 20, 2026. It is 2.08% discount to the five-day volume weighted average (VWAP) price of RM4.851 up to and including May 20.

Following completion of the exercise, LPI and Lonpac no longer hold any shares in PBBANK.

The disposal was carried out in compliance with regulatory requirements under Section 22(5)(b) of the Financial Services Act. On completion of the disposal, LPI Capital and subsidiary Lonpac Insurance no longer hold shares in PBBANK thereby satisfying the cross-shareholdings restrictions between subsidiaries and parent companies.

For LPI Capital, the disposal mandate outlined that approximately 70% of the gross proceeds would be earmarked to reward shareholders of as special cash dividends. The remaining balance of the proceeds will be retained to support the company’s investment portfolio and future business growth.

Selldown of 50 million shares by Consolidated Teh

Further to their announcement on 10/10/24, the Estate of the late Tan Sri Teh Hong Piow (via Consolidated Teh Holdings Sdn Bhd) has announced the disposal of 50 million shares (0.26%) in Public Bank Bhd. The date of change was shown as 8/10/25. The Teh family still holds over 22% of the banking group after the sell down. The family is required to gradually reduce its stake to 10% within five years through a restricted offer for sale (ROFS) to comply with the Financial Services Act. Which means it still needs to sell down well over 2 billion shares over the next 4 years or over 500 million shares each year on average.

Public Bank shares closed at RM4.34 on 8/10/25 with 4.9 million shares traded at a range of RM4.31 to 4.34.

Goodwill Impairment for Public Bank

Public Bank Bhd’s upcoming Q4 results, scheduled for release on 26/2/25, are expected to reflect the financial impact of the goodwill impairment at its 73.2%-owned subsidiary, Public Financial Holdings (PFH), which had recorded a goodwill impairment on its wholly owned subsidiaries, Public Bank (HK) Ltd, Public Finance Ltd, and Winton (BVI) Ltd. The impairment was approximately HK$810 million or RM463 million.

(Source: TheEdge)

Public Bank Completion of LPI Acquisition

Public Bank (PBB) completed its acquisition of a 44.15% stake in LPI Capital (LPI) in December 2024, acquiring it from the estate of Tan Sri Teh Hong Piow and his private vehicle, Consolidated Teh Holdings Sdn Bhd. This acquisition was for a total of RM1.72 billion in cash, or RM9.80 per share. As a result, PBB now holds a controlling stake* in LPI.

Key Details:

Acquisition: PBB acquired a 44.15% stake in LPI Capital.

Value: The acquisition was valued at RM1.72 billion in cash, or RM9.80 per share which is 1.71x LPI’s book value and 12.4x 2023 earnings.

The stake was acquired from the Estate of Tan Sri Teh Hong Piow and Consolidated Teh Holdings Sdn Bhd.

LPI share price closed at RM13.14, while PBB at RM4.53 at completion of the acquisition on 4/12/25.

Consequences of the Acquisition:

- Public Bank now holds a controlling stake in LPI, giving it greater influence over its operations.

- As a subsidiary of Public Bank, LPI is required to dispose of its 1.1% stake in PBB within 12 months due to the acquisition.

- The sale of Public Bank shares by LPI could potentially lead to special dividends for LPI shareholders, some estimates suggest RM1.89 per share.

- The acquisition aligns with PBB’s strategy to enhance its presence in the insurance sector through LPI, a leading general insurer in Malaysia.

- Some analysts expect the acquisition to be earnings accretive for Public Bank, potentially boosting group earnings by around 2%

*PBB considers that it controls LPI Capital Bhd (“LPI”) even though it owns less than 50% of the voting rights. This is because the Group is the single largest shareholder of LPI with a 44.15% equity interest. The remaining 55.85% of the equity shares in LPI are widely held by many other shareholders, none of which individually hold more than 10% of the equity shares (as recorded in the company’s shareholders’ register on 4 December 2024. Since the date of acquisition of LPI on 4 December 2024, there has been no history of the other shareholders collaborating to exercise their votes collectively or to outvote the Group.

Source: Public Bank Berhad 2024 Integrated Annual Report Financial Statements P39.

Public Bank Acquisition of Lonpac and Teh Family Divestment

On 10/10/24 it was reported that Public Bank Bhd would acquire 44.15% stake in LPI Capital for RM1.72bil by launching a Mandatory General Offer for LPI at RM9.80/share.

Teh Li Shian Diona, daughter of the late Tan Sri Dr Teh Hong Piow also announced that the Estate and Consolidated Teh Holdings Sdn Bhd intended to undertake a restricted offer for sale of a portion of their Public Bank shares over a 5-year period, in compliance with the Financial Services Act. The acquisition of 44.15% in LPI Capital (175.9 million shares) was completed on 4/12/24.

To honour the late founder’s legacy and in appreciation to key stakeholders, Consolidated Teh will divest a portion of its Public Bank shares at a discount to all employees, directors and eligible shareholders of the Public Bank Group. According to Diona Teh, “this initiative aims to ensure that Public Bank remains in the hands of those who have nurtured its growth and success over the years, enabling us to continue building our legacy together,”